How banks and processors win the SMB relationship against software platforms

Market Context

Merchant services has become one of the most important competitive battlegrounds in small business banking. Software-led platforms have demonstrated that controlling payments is not just about processing transactions, but about anchoring the broader SMB relationship.

The scale of the opportunity is substantial. The SMB acquiring market represents approximately USD 25 billion in annual revenue, with a further USD 18 billion available through terminals and SaaS fees, and significantly more when downstream banking products are considered.

Merchant services are a strategic lever for deepening business relationships and driving revenue. Business customers using these services hold deposits twice as large, driving higher interest income and greater loyalty.

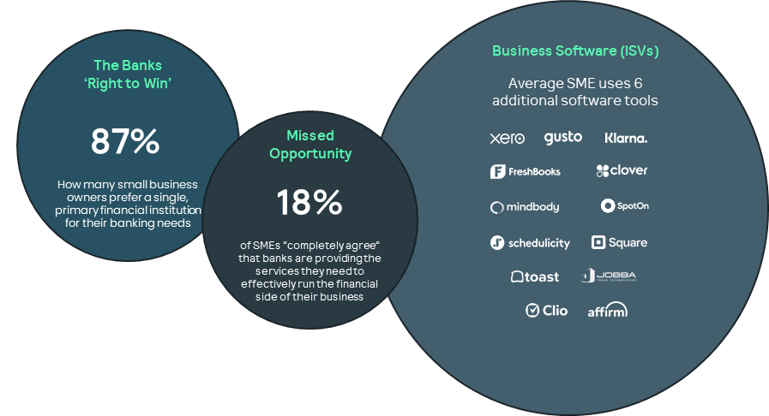

Despite this, banks are standing idle while their market share in acquiring continues to fall (58% to 43%) vs digital first competitors. These challengers are now expanding into broader financial services: for instance, Toast now generates 67% of its profits from banking products, with 55% directly linked to payments.

Software’s Winning Formula

These platforms embed payments directly into core business workflows such as point of sale, invoicing, inventory management, and staff management, removing the need for separate systems or external portals. Onboarding is frictionless and typically completed in minutes, with minimal data entry, transparent pricing, and immediate access to terminals, gateways, and reporting.

Merchant services is positioned as a default capability rather than a specialist product, with integrated hardware, software, and support delivered through a single provider.

Once established, these platforms expand the relationship through adjacent services including lending, cards, and accounts receivable and payable, using transaction data to personalise offers and deepen engagement. This integrated model is translating into rapid adoption and market share gains.

The Opportunity for Banks

Merchant services represents one of the most powerful and underutilised value levers in small business banking. The opportunity extends well beyond acquiring margin and touches revenue growth, balance sheet quality, operating efficiency, and long-term customer value.

At a direct level, merchant services generates highly recurring, transaction-linked income that scales with customer activity. Payments, terminals, and adjacent services such as invoicing and value-added tools provide durable fee-based revenue at a time when balance sheet growth is increasingly constrained.

At the same time, merchant services materially strengthens the broader banking relationship. Business customers that adopt merchant services hold significantly higher deposit balances, exhibit lower attrition, and demonstrate greater lifetime value across lending, treasury, and card products. Payments data also enables more relevant cross-sell and more informed credit and cash management decisions.

Modern merchant services propositions create meaningful leverage. Digital onboarding and self-service reduce manual effort, lower cost to serve, and free specialist teams to focus on higher-value client relationships. Integrated experiences also open new acquisition channels, allowing relationship managers and branch staff to capture demand at the point of need rather than referring customers elsewhere.

Strategically, merchant services plays a critical defensive role. As software platforms use payments to anchor broader operating ecosystems, banks that fail to compete at the experience layer risk losing relevance across the SMB relationship. Those that succeed position themselves as the primary financial partner for small businesses, with payments acting as the gateway to deeper engagement and sustained growth.

Challenges to Overcome

Yet despite the opportunity, merchant services penetration across bank-led FI programmes remains low, typically around 2–5% of business banking customers. Different operating models deliver very different outcomes, with referral-style models rarely exceeding low single-digit penetration, bank-owned models reaching 5–15%, and best-in-class integrated propositions achieving materially higher adoption.

The challenge is not processing capability or lack of market demand, but how merchant services is delivered. Most FI propositions are still powered by outsourced, processor-led technology that sits outside the bank’s digital channels and carries third-party branding.

This results in fragmented customer journeys and limits the bank’s ability to differentiate its proposition or meet rising customer expectations for integrated financial services. Onboarding remains slow and manual, often requiring merchants to re-enter information the bank already holds, with many institutions still directing customers to call centres operating limited hours and onboarding journeys that take days or weeks rather than minutes.

This operating model does not scale. Payment advisors spend disproportionate time manually boarding low-value merchants and responding to basic service queries that could be self-served, reducing their capacity to focus on higher-value SMBs that require consultative, white-glove support. Branch teams are largely excluded from direct selling due to lack of tooling and integration, while merchants experience payments as a disconnected add-on rather than a core part of their banking relationship.

As a result, penetration remains structurally capped, cost to serve remains high, and banks and processors struggle to respond as software platforms continue to raise the bar on speed, integration, and breadth of services.

A third option exists where a bank or processor has a strong strategic focus or existing strength within a particular vertical. In these cases, building or acquiring a specialised software capability can be a viable way to accelerate ecosystem ownership. An example is PNC acquiring Linga to deepen its position in restaurant and hospitality payments. This approach requires clear vertical conviction and long-term commitment, but can create defensible differentiation when executed well.

The common thread across all three paths is that success depends less on processing capability and more on delivering the right experience in the right context. In reality, there will be a compromise, and successful banks will identify and prioritise certain verticals in line with their own customer growth strategy. Banks and processors do not need a single strategy for all merchants, but they do need a deliberate approach that aligns customer expectations, experience ownership, and economic outcomes.